2012 Legislative Session

| | FLORIDA SUPREME COURT |

November 11, 2012 - The Florida Supreme Court has delegated to The Florida Bar, as an official arm of the court, the duty to investigate and prosecute allegations of unauthorized practice of law (UPL). One statewide Standing Committee on Unlicensed Practice of Law supervises circuit committees (which investigate reports of unlicensed practice and report their findings to the statewide standing committee). It also issues formal advisory opinions on whether specific conduct constitutes the unlicensed practice of law which are then filed with the Supreme Court of Florida.

| | GEORGE MEYER |

On March 28, 2012, Chairman George Meyer of the Real Property, Probate and Trust Law Section of The Florida Bar (RPPTL Section) sent a request to the Standing Committee on the Unauthorized Practice of Law of The Florida Bar to determine whether certain activities constitute the unauthorized practice of law when performed by Community Association Managers. Mayer was seeking an update. In 1996, the Florida Supreme Court affirmed an earlier advisory opinion issued by the Committee in �The Florida Bar re: Advisory Opinion-Activities of Community Association Managers, 681 So.2d 1189 (Fla. 1996).� On March 28, 2012, Chairman George Meyer of the Real Property, Probate and Trust Law Section of The Florida Bar (RPPTL Section) sent a request to the Standing Committee on the Unauthorized Practice of Law of The Florida Bar to determine whether certain activities constitute the unauthorized practice of law when performed by Community Association Managers. Mayer was seeking an update. In 1996, the Florida Supreme Court affirmed an earlier advisory opinion issued by the Committee in �The Florida Bar re: Advisory Opinion-Activities of Community Association Managers, 681 So.2d 1189 (Fla. 1996).�

Since then, Florida Courts have deemed that the following actions - if undertaken by a licensed CAM Manager - constitute the unauthorized practice of law: I) drafting a claim of lien; drafting a satisfaction of lien; II) preparing a notice of commencement; drafting a frequently asked question and answer sheet; preparing amendments to the declaration, articles of incorporation, or the bylaws; III) determining the timing, method and form of giving notices of meetings; IV) determining the votes necessary for certain actions by community associations; V) addressing questions asking for the application of a statute or rule; and VI) advising community associations whether a course of action is authorized by statute or rule. The Court further identified a �grey area� which involved activities that may or may not constitute the practice of law depending upon the relevant facts. Since then, Florida Courts have deemed that the following actions - if undertaken by a licensed CAM Manager - constitute the unauthorized practice of law: I) drafting a claim of lien; drafting a satisfaction of lien; II) preparing a notice of commencement; drafting a frequently asked question and answer sheet; preparing amendments to the declaration, articles of incorporation, or the bylaws; III) determining the timing, method and form of giving notices of meetings; IV) determining the votes necessary for certain actions by community associations; V) addressing questions asking for the application of a statute or rule; and VI) advising community associations whether a course of action is authorized by statute or rule. The Court further identified a �grey area� which involved activities that may or may not constitute the practice of law depending upon the relevant facts.

�What's the big deal?� To begin with, UPL is a criminal offense in the State of Florida � a misdemeanor of the first degree, which is punishable by up to one year in jail and a fine of up to one thousand dollars for each violation. Additionally, insurance or contractual indemnification provisions that might ordinarily shield management personnel are often inapplicable to criminal activity. A CAM Manager could also forfeit the license that puts food on the table. �What's the big deal?� To begin with, UPL is a criminal offense in the State of Florida � a misdemeanor of the first degree, which is punishable by up to one year in jail and a fine of up to one thousand dollars for each violation. Additionally, insurance or contractual indemnification provisions that might ordinarily shield management personnel are often inapplicable to criminal activity. A CAM Manager could also forfeit the license that puts food on the table.

Responding to Mayer�s request, the Committee examined 14 specific activities for prospective infractions. Following a June 22, 2012 public hearing in Orlando, a phalanx of Community Association advocates, board members and unit owners expressed conflicting opinions about: the actual findings, the impact on association budgets, and the underlying rationale for this review, given the negligible abuse reported by the DBPR. Thinly veiled intimations of turf protection linked all the recorded feedback, as each contributor diplomatically danced around a brazen conflict of interest beclouding the Committee�s motives. Responding to Mayer�s request, the Committee examined 14 specific activities for prospective infractions. Following a June 22, 2012 public hearing in Orlando, a phalanx of Community Association advocates, board members and unit owners expressed conflicting opinions about: the actual findings, the impact on association budgets, and the underlying rationale for this review, given the negligible abuse reported by the DBPR. Thinly veiled intimations of turf protection linked all the recorded feedback, as each contributor diplomatically danced around a brazen conflict of interest beclouding the Committee�s motives.

| | DONNA BERGER |

Community Advocacy Network (CAN) Executive Director Donna Berger exclaimed that the issues being considered demonstrate a �real disconnect between what constitutes �practicing law� and what constitutes �following the law�.� Opposed to creating �an arbitrary or petty list of activities or decisions� that must have a legal opinion; Berger said that some of the attorneys promoting these changes were guilty of �overkill or territorialism.� Miffed by the Committee�s arbitrary decision to hold a single public hearing to elicit input from 60,000 Community Associations that employ 15,600 CAM Managers in all parts of the state, Community Associations Institute (CAI) CEO Thomas Skiba cynically inquired �What is the basis for these concerns and could it be perceived as simply related to billable hours and fees?�

| | CAI CEO THOMAS SKIBA |

Marginalizing complaints about nest feathering, the Committee�s �peers� in the Florida Bar�s Real Property, Probate and Trust Law (RPPTL) Section observed �No evidence has been presented to support a conclusion that the cost will be so large as to penalize a community, especially considering the cost of correcting problems resulting from the unauthorized practice of law.� Resorting to an upscale version of the nursery school enigma �I know you are but what am I,� newly seated RPPTL Chair William Fletcher Belcher reduced the issue to a sophomoric whizzing contest between managers and lawyers, announcing �In response to the argument raised by some that the Section�s request is designed to increase our attorney revenues, one might just as easily say that Licensed Community Association Managers� comments are motivated by their own financial interests.�

Unconcerned about civility or collegiality, comments by angry Board members, officers and unit owners were exemplified by East Lake Woodlands resident Alan F. Gomber � an insulin dependent diabetic whose condo lost 50% of its value in 4 years � who noted �I�m already at the point where I have to make a daily decision on whether to eat or take my medications. And now your money-grubbing �fraternity� wants to hammer us with a policy that will result in further severe economic hardship. What a joke--hope y�all can sleep well knowing how much pain and suffering all that extra money in your bank account is going to bring upon us peons. As William Shakespeare wrote, �Kill all the lawyers--kill �em tonight!� AMEN.� Unconcerned about civility or collegiality, comments by angry Board members, officers and unit owners were exemplified by East Lake Woodlands resident Alan F. Gomber � an insulin dependent diabetic whose condo lost 50% of its value in 4 years � who noted �I�m already at the point where I have to make a daily decision on whether to eat or take my medications. And now your money-grubbing �fraternity� wants to hammer us with a policy that will result in further severe economic hardship. What a joke--hope y�all can sleep well knowing how much pain and suffering all that extra money in your bank account is going to bring upon us peons. As William Shakespeare wrote, �Kill all the lawyers--kill �em tonight!� AMEN.�

On September 21, 2012, after voting to submit the final advisory opinion to the Florida Supreme Court, the Committee waffled, adding that it might later vote to not to submit their handiwork. During the meeting, the Committee determined whether a manager performing each of the following 14 activities is or is not engaged in the unlicensed practice of law (UPL). They range from the obvious to the ridiculous. On September 21, 2012, after voting to submit the final advisory opinion to the Florida Supreme Court, the Committee waffled, adding that it might later vote to not to submit their handiwork. During the meeting, the Committee determined whether a manager performing each of the following 14 activities is or is not engaged in the unlicensed practice of law (UPL). They range from the obvious to the ridiculous.

Preparation of a certificate of assessments due once the delinquent account has been turned over to the association�s attorney (committee determined this IS NOT UPL). Preparation of a certificate of assessments due once the delinquent account has been turned over to the association�s attorney (committee determined this IS NOT UPL).

Preparation of a certificate of assessments due once a foreclosure against the unit has commenced (committee determined this IS NOT UPL).

Preparation of a certificate of assessment due once a member disputes in writing to the association the amount alleged as owed (committee determined this IS NOT UPL).

Drafting amendment (and certificates of amendment that are recorded in the official records) to a declaration of covenants, bylaws, or articles of incorporation when such documents are to be voted on by the members (committee determined this IS UPL). Drafting amendment (and certificates of amendment that are recorded in the official records) to a declaration of covenants, bylaws, or articles of incorporation when such documents are to be voted on by the members (committee determined this IS UPL).

Determination of the number of days to be provided for a statutory notice (committee determined this IS UPL).

Modification of limited proxy forms promulgated by the State (requires further clarification � depends on the definition of �modifications� and whether they are ministerial � typos, etc. � or require legal opinions.

Preparation of documents concerning the right of the association to approve new prospective owners (requires further clarification � Specifically, whether the drafting of forms to be completed by prospective owners constitute UPL.) Preparation of documents concerning the right of the association to approve new prospective owners (requires further clarification � Specifically, whether the drafting of forms to be completed by prospective owners constitute UPL.)

Determination of affirmative votes needed to pass a proposition or amendment to recorded documents (committee determined this IS UPL).

Determination of owners� votes needed to establish a quorum (committee determined this IS UPL).

Drafting of pre-arbitration demand letters required by 718.1255, Fla. Statutes. (although not considered in 1996, the Committee will refer to the 1996 opinion for guidance)

Preparation of construction lien documents � such as a notice of commencement, lien waivers, etc. (committee determined this IS UPL).

Preparation, review, drafting, and/or substantial involvement in the preparation or execution of contracts, including construction contracts, management contracts, cable television contracts, etc. (committee determined this IS UPL). Preparation, review, drafting, and/or substantial involvement in the preparation or execution of contracts, including construction contracts, management contracts, cable television contracts, etc. (committee determined this IS UPL).

Identifying, through review of title instruments, the owners to receive pre-lien letters (also not considered in 1996, whether or not a manager could/should review title instruments will presumably be addressed at a future Committee meeting)

Any activity that requires statutory or case law analysis to reach a legal conclusion (committee determined this IS UPL).

Although not yet scheduled, the next meeting of the Standing Committee on the Unauthorized Practice of Law of The Florida Bar is expected to take place sometime in mid-February 2013. Although the process is technically closed to further input, since many attorneys have divergent opinions about the necessity or advisability of pursuing this effort, if and in what form the opinion is ultimately submitted to the Florida Supreme Court is a crap shoot. Although not yet scheduled, the next meeting of the Standing Committee on the Unauthorized Practice of Law of The Florida Bar is expected to take place sometime in mid-February 2013. Although the process is technically closed to further input, since many attorneys have divergent opinions about the necessity or advisability of pursuing this effort, if and in what form the opinion is ultimately submitted to the Florida Supreme Court is a crap shoot.

| DR. ANTHONY B. SPIVEY - DBPR

CAM REGULATORY COUNCIL |

While the opinion targets Community Association Managers, board members who perform tasks and actions considered by the Florida Supreme Court as the unauthorized practice of law aren�t exempt from legal consequences. The significant training and experience that CAM Managers bring to the table prompted Dr. Anthony B. Spivey, Executive Director for the Regulatory Council of Community Association Managers at the DBPR, to oppose some committee decisions and support a manager�s performance of items 1, 2, 3, 5, 7, 8 and 9 without reservation. Requiring a lawyer to determine the number of votes needed for a quorum or the number of days required for notice, as described in the governing documents, is a blatantly self-benefitting fiscal abuse.

Conversely, since most Board members are marginally qualified, the Committee�s findings become far more credible when applied to volunteer directors who tender legal opinions for their associations. Although they don�t risk a professional license, Board members whose frivolous legal decisions drive up association costs could reasonably be perceived as violating their fiduciary responsibility. As with a manager�s contractual protections, the directors� and officers� insurance that fortifies the indemnification provisions in the association�s governing documents may not protect directors found culpable of criminal activity. A word to the wise... Conversely, since most Board members are marginally qualified, the Committee�s findings become far more credible when applied to volunteer directors who tender legal opinions for their associations. Although they don�t risk a professional license, Board members whose frivolous legal decisions drive up association costs could reasonably be perceived as violating their fiduciary responsibility. As with a manager�s contractual protections, the directors� and officers� insurance that fortifies the indemnification provisions in the association�s governing documents may not protect directors found culpable of criminal activity. A word to the wise...

Click To Top of Page

A Constitutional Junkyard

11 Amendments on the 2012 Florida Ballot

The Process

October 23, 2012 - Of the five methodologies available to amend the Florida Constitution, citizen initiative petitions and legislative Joint Resolutions (SJR, HJR) are the most common. When stonewalled by lawmakers, citizens can place an amendment on the ballot by collecting petition signatures equal in number to 8% of the votes cast in the last Presidential election and sourced from at least one-half of the State�s Congressional Districts. In the November 2010 election, 63% of the voters successfully used this format to fit the Florida Constitution with new redistricting standards that replaced nearly two centuries of cultural reassignment, racial gerrymandering and partisan vote dilution with district lines based on factors unrelated to party and incumbency. October 23, 2012 - Of the five methodologies available to amend the Florida Constitution, citizen initiative petitions and legislative Joint Resolutions (SJR, HJR) are the most common. When stonewalled by lawmakers, citizens can place an amendment on the ballot by collecting petition signatures equal in number to 8% of the votes cast in the last Presidential election and sourced from at least one-half of the State�s Congressional Districts. In the November 2010 election, 63% of the voters successfully used this format to fit the Florida Constitution with new redistricting standards that replaced nearly two centuries of cultural reassignment, racial gerrymandering and partisan vote dilution with district lines based on factors unrelated to party and incumbency.

Other vehicles for placing amendments on the ballot are a Constitutional Convention, a Constitutional Revision Commission and the Taxation and Budget Reform Committee. If approved by a simple majority in an election, voters can call a Constitutional Convention to consider and propose amendments. The Constitutional Revision Commission is comprised of the State Attorney General, 15 members selected by the Governor of Florida, 9 each by the Statehouse Speaker and Senate President and 3 by the Chief Justice of the Florida Supreme Court. The 37-member panel meets every 20 years (last in 1997) to consider and propose amendments. Other vehicles for placing amendments on the ballot are a Constitutional Convention, a Constitutional Revision Commission and the Taxation and Budget Reform Committee. If approved by a simple majority in an election, voters can call a Constitutional Convention to consider and propose amendments. The Constitutional Revision Commission is comprised of the State Attorney General, 15 members selected by the Governor of Florida, 9 each by the Statehouse Speaker and Senate President and 3 by the Chief Justice of the Florida Supreme Court. The 37-member panel meets every 20 years (last in 1997) to consider and propose amendments.

Created in 2007 to adapt tax strategies to the deepening recession and also convened every 20 years, Taxation and Budget Commission meetings are staggered with those of the Constitutional Revision Commission, providing a reliable opportunity to amend the Florida Constitution every 10 years. Of the 25-member Commission, which includes no sitting lawmakers, 11 are selected by the Governor, 7 each by the Statehouse Speaker and Senate President, who also each select 2 legislators (one from each side of the aisle) to serve as �ex officio� members. Created in 2007 to adapt tax strategies to the deepening recession and also convened every 20 years, Taxation and Budget Commission meetings are staggered with those of the Constitutional Revision Commission, providing a reliable opportunity to amend the Florida Constitution every 10 years. Of the 25-member Commission, which includes no sitting lawmakers, 11 are selected by the Governor, 7 each by the Statehouse Speaker and Senate President, who also each select 2 legislators (one from each side of the aisle) to serve as �ex officio� members.

Vengeance

Since many Florida Legislators view constitutional dictums as personal playthings, the reforms in Amendments 5 and 6 drove many incredulous elected officials into a blended state of apoplexy and depression. No longer able to preselect who could vote in the districts where they planned to run, politicians were suddenly forced to leave election outcomes to voters, often for the first time in their public service careers. While outraged lawmakers complained bitterly about a process that allowed ordinary people to mess with their career paths by leveling long-twisted playing fields, legislative leaders explored plans to give the arrogant public a taste of its own medicine. Since many Florida Legislators view constitutional dictums as personal playthings, the reforms in Amendments 5 and 6 drove many incredulous elected officials into a blended state of apoplexy and depression. No longer able to preselect who could vote in the districts where they planned to run, politicians were suddenly forced to leave election outcomes to voters, often for the first time in their public service careers. While outraged lawmakers complained bitterly about a process that allowed ordinary people to mess with their career paths by leveling long-twisted playing fields, legislative leaders explored plans to give the arrogant public a taste of its own medicine.

This year, Republican legislators cobbled together several failed bills that repeatedly collapsed under Committee Review or public scrutiny. Using partisan pressure to eke out a two-thirds majority in both houses, they prepared 11 Joint Resolutions for ballot eligibility. Since the legislative ballot process involves negligible public participation, politicians could promote or support openly anathematic issues with little fear of political reprisal or constituent backlash. Few voters would check to see which officials created the amendments, much less who voted for them. This year, Republican legislators cobbled together several failed bills that repeatedly collapsed under Committee Review or public scrutiny. Using partisan pressure to eke out a two-thirds majority in both houses, they prepared 11 Joint Resolutions for ballot eligibility. Since the legislative ballot process involves negligible public participation, politicians could promote or support openly anathematic issues with little fear of political reprisal or constituent backlash. Few voters would check to see which officials created the amendments, much less who voted for them.

To shield highly controversial amendments from suffering the same fatal public scrutiny that buried the snake-bit bills from which they were sourced, they were added to a fistful of sympathetic yet poorly timed tax exemptions and a few amendments so fatuous that Constitutional watchdogs on both sides of the aisle concede them as �filler�. Pumping out almost a dozen garrulous amendments would insure that impatient voters would tick off �yes� or �no� based on little more than a deliberately misleading ballot title. To shield highly controversial amendments from suffering the same fatal public scrutiny that buried the snake-bit bills from which they were sourced, they were added to a fistful of sympathetic yet poorly timed tax exemptions and a few amendments so fatuous that Constitutional watchdogs on both sides of the aisle concede them as �filler�. Pumping out almost a dozen garrulous amendments would insure that impatient voters would tick off �yes� or �no� based on little more than a deliberately misleading ballot title.

Since you will doubtless be preoccupied with selecting a President, a U.S. Senator, a Congressperson, a Florida Senator, a Statehouse Representative and some Judges when finally faced with a ballot, by reading the following summary, you�ll be able to whiz through the 11 prospective changes to Florida�s Constitution � without inadvertently emptying your wallet.

Amendment 1: Health Care Services

Amendment 1 seeks to prohibit the government from requiring individuals or employers to purchase health insurance. (SJR 2 � sponsored in 2011 by Sen. Mike Haridopolos, R-Merritt Island, and Rep. Scott Plakon, R-Longwood) Amendment 1 seeks to prohibit the government from requiring individuals or employers to purchase health insurance. (SJR 2 � sponsored in 2011 by Sen. Mike Haridopolos, R-Merritt Island, and Rep. Scott Plakon, R-Longwood)

- Since the U.S. Supreme Court on June 28, 2012, upheld the constitutionality of the �individual mandate� (i.e. ObamaCare), passage or defeat of this amendment will have no impact on the Florida Constitution. When federal and state laws conflict, the Supremacy Clause of the U.S. Constitution affirms the federal government as �supreme law of the land,� relegating Amendment 1 to a partisan dog and pony show.

- By the way, Florida has the second highest rate (24%) of uninsured citizens in the United States. That�s citizens � not undocumented workers (�illegals�). When taken ill, the emergency rooms they turn to for treatment cost an average $1318 per visit. If insured, the same treatment in a doctor�s office costs an average $188 per visit. Either way, we pick up the tab.

Amendment 2: Veterans Disabled Due to Combat Injury; Homestead Property Tax Discount

Amendment 2 would provide disabled veterans who were not Florida residents prior to entering military service with a discount on their property taxes. A 2006 amendment that provides the exemption to veterans who lived in Florida prior to joining the military would be expanded to those who moved here later in life. If passed, this amendment would cost local governments $15 million over the first three years of implementation. (SJR 592 � sponsored by Sen. Mike Bennett, R-Bradenton, and Rep. Doug Holder, R-Sarasota) Amendment 2 would provide disabled veterans who were not Florida residents prior to entering military service with a discount on their property taxes. A 2006 amendment that provides the exemption to veterans who lived in Florida prior to joining the military would be expanded to those who moved here later in life. If passed, this amendment would cost local governments $15 million over the first three years of implementation. (SJR 592 � sponsored by Sen. Mike Bennett, R-Bradenton, and Rep. Doug Holder, R-Sarasota)

- This is the first of five amendments constructed around the same formula �

disparate groups of sympathetic homeowners are fitted with an assortment of property tax exemptions. Since local governments burned through their reserves in the past few years and have already cut services to the bone, there is no more �low hanging fruit� available to offset deficits. For those amendments that tug on your heart strings, you must decide whether you want to pay for them before casting your vote. Although everyone appreciates our veterans, while we are forced to close parks and libraries may not be the best time to invite them here from all over the country and subsidize their living expenses. YOU will pay the tax burden created by the shortfall. disparate groups of sympathetic homeowners are fitted with an assortment of property tax exemptions. Since local governments burned through their reserves in the past few years and have already cut services to the bone, there is no more �low hanging fruit� available to offset deficits. For those amendments that tug on your heart strings, you must decide whether you want to pay for them before casting your vote. Although everyone appreciates our veterans, while we are forced to close parks and libraries may not be the best time to invite them here from all over the country and subsidize their living expenses. YOU will pay the tax burden created by the shortfall.

Amendment 3: State Government Revenue Limitation

- Amendment 3 would base an annual state revenue limit on a formula that considers population growth and inflation instead of the current method that uses personal income to calculate the revenue limit. While this alternative cap would supposedly lower revenues, it comes with a built-in set of legislative loopholes that exempt certain revenue streams or completely circumvent the cap � defeating the amendment�s objective. Rejected in many states across the country, the only state where this schizophrenic formula was implemented is Colorado, where lawmakers were later forced to dump the restrictions when they threatened essential public services such as health care, transportation and education. Economists agree that the formula is inherently unworkable because it precludes the State from funding new growth. However, it�s perfect if the objective is simply to crowd the ballot with junk amendments. (SJR 958 � sponsored in 2011 by Sen. Ellyn Bogdanoff, R-Fort Lauderdale, and Rep. Steve Precourt, R-Orlando)

Amendment 4: Property Tax Limitations; Property Value Decline; Reduction for Non-homestead Assessment Increases; Delay of Scheduled Repeal

Amendment 4 would reduce the maximum annual increase in taxable value of non-homestead properties from 10 percent to 5 percent; provide an extra homestead exemption for first-time home buyers; allow lawmakers to prohibit assessment increases for properties with decreasing market values. (HJR 381 � sponsored in 2011 by Sen. Mike Fasano, R-New Port Richey, and Rep. Chris Dorworth, R-Lake Mary) Amendment 4 would reduce the maximum annual increase in taxable value of non-homestead properties from 10 percent to 5 percent; provide an extra homestead exemption for first-time home buyers; allow lawmakers to prohibit assessment increases for properties with decreasing market values. (HJR 381 � sponsored in 2011 by Sen. Mike Fasano, R-New Port Richey, and Rep. Chris Dorworth, R-Lake Mary)

- No amendment more dramatically demonstrates the zero-sum nature of tax policy. Revenues lost to local governments by lowering the cap for non-resident property owners (snowbirds), landlords and businesses from 10% to 5% will trigger a sizable tax increase or serious service cuts.

| | BOB WOLFE OF BCPA |

Of far greater consequence is a startlingly generous additional exemption (up to $150,000 added to the existing $50,000 homestead exemption) for anyone who hadn�t applied for a homestead exemption in the prior 3 years. The exemption would equal 50% of the median just value of a property and diminish by 20% each year over a five year period. However, instead of attracting more first time home buyers, Bob Wolfe of the Broward County Property Appraiser�s Office (BCPA) warned that unscrupulous speculators could easily milk the poorly drafted freebie by making acquisitions in the names of unpropertied family members. Intimately familiar with the kind of regulatory language that invites tax fraud, Wolfe laments the decision by lawmakers to muddy the Constitution with obtuse piecemeal tax policies instead of making balanced statutory changes to the tax code.

- Generally misconstrued as an eerie glitch in the tax code, despite plunging valuations, thousands of properties (71,000 in Broward this year) were tagged with miniscule tax increases resulting from the statutory �Save our Homes� (SOH) Recapture Rule, which this amendment would eliminate. As expressed by Wolfe, this reasonable change was added to sweeten the wallet-crushing parts of this amendment.

Buried in this Rube Goldberg exemption grab bag is an embarrassingly fat tax increase. While zapping the Recapture Rule may only cost a few $million in revenues, the amendment�s other major giveaways will add over $1.7 billion to local government deficits within four years, forcing up local millage (tax) rates or cuts to critical services. Buried in this Rube Goldberg exemption grab bag is an embarrassingly fat tax increase. While zapping the Recapture Rule may only cost a few $million in revenues, the amendment�s other major giveaways will add over $1.7 billion to local government deficits within four years, forcing up local millage (tax) rates or cuts to critical services.

Amendment 5: State Courts

Amendment 5 would provide the Senate with approval power over Supreme Court justices appointed by the Governor; gives lawmakers power to change rules governing the court system by a simple majority in both houses instead of the current 2/3 majority; enables lawmakers to repeal Judicial Nominating Commission and Judicial Qualifications Commission rules by a majority of those legislators �present� instead of an actual legislative majority; direct the Judicial Qualifications Commission, which investigates judicial misconduct complaints, to make its files available to the Speaker of the Florida House of Representatives whether or not the request is specifically related to impeachment consideration. (HJR 7111 � sponsored in 2011 by House and Senate Judiciary Committees, and Rep. Eric Eisnaugle, R-Orlando) Amendment 5 would provide the Senate with approval power over Supreme Court justices appointed by the Governor; gives lawmakers power to change rules governing the court system by a simple majority in both houses instead of the current 2/3 majority; enables lawmakers to repeal Judicial Nominating Commission and Judicial Qualifications Commission rules by a majority of those legislators �present� instead of an actual legislative majority; direct the Judicial Qualifications Commission, which investigates judicial misconduct complaints, to make its files available to the Speaker of the Florida House of Representatives whether or not the request is specifically related to impeachment consideration. (HJR 7111 � sponsored in 2011 by House and Senate Judiciary Committees, and Rep. Eric Eisnaugle, R-Orlando)

| HOUSE SPEAKER

DEAN CANNON |

This is a bald-face attempt to make Florida�s Judiciary subservient to its Legislature, fatally skewing the traditional balance of power. Although the U.S. Senate confirms Supreme Court nominees, federal justices receive lifetime appointments. Since state justices are subject to merit retention votes, requiring Senate approval simply erodes Judiciary independence and Executive appointment powers.

- Dropping the currently required two-thirds majority to repeal court rules adopted by the State Supreme Court to a simple majority will empower a majority political party to unilaterally engineer control over the courts. This amendment is actually a summary of screwball changes filed in 2011 by House Speaker Dean Cannon (R-Winter Park), who originally proposed adding three justices to the Supreme Court and then split the court into two five-member panels, respectively hearing criminal and civil cases. Cannon saw no problem with Florida being the only state without a viable Judiciary. The Chief Justice could always sell fajitas in the gallery.

Amendment 6: Prohibition on Public Funding of Abortions; Construction of Abortion Rights

| | AMENDMENT SPONSOR OCALA REPRESENTATIVE DENNIS BAXLEY |

Amendment 6 would make the existing federal ban on public funding for most abortions part of the state constitution. It would narrow the scope of a state privacy law that is sometimes used in Florida to challenge abortion laws. (HJR 1179 � sponsored in 2011 by Sen. Anitere Flores, R-Miami, and Rep. Dennis Baxley, R-Ocala)

- Whether or not one agrees with the federal law that affirms the reproductive rights of women, this attempt to thwart established law by submarining a 1980 voter mandated privacy rights constitutional protection is a dangerous slippery slope. Although Sponsor Rep. Dennis Baxley stated that he was primarily concerned about the cost of taxpayer-funded abortions, he spent more on one ad explaining the amendment than the total $534.60 paid for abortions with tax dollars in fiscal year 2009-10. Being forced to sacrifice constitutionally guaranteed rights to fight terrorism is a tough pill to swallow. Sacrificing those rights in order to monkey wrench legal abortions borders on the ridiculous.

Amendment 8: Religious Freedom (Originally known as Amendment 7 until a legal challenge forced the Attorney General to redraft the ballot language, after which it was reinstated on the ballot as Amendment 8 � thereby accounting for the mysterious absence of an Amendment 7.)

Amendment 8 would remove the prohibition in Florida�s Constitution that prevents religious institutions from receiving taxpayer funding. (HJR 1471 � sponsored in 2011 by Sen. Thad Altman, R-Melbourne, Rep. Scott Plakon, R-Longwood, and Rep. Steve Precourt, R-Orlando) Amendment 8 would remove the prohibition in Florida�s Constitution that prevents religious institutions from receiving taxpayer funding. (HJR 1471 � sponsored in 2011 by Sen. Thad Altman, R-Melbourne, Rep. Scott Plakon, R-Longwood, and Rep. Steve Precourt, R-Orlando)

- Previously removed from the 2008 ballot, Amendment 8 would eliminate a long-established tenet underscoring the separation of church and state, the constitutional pillar upon which the Country�s �Founding Fathers� grounded religious freedom. By reversing a 126-year old prohibition against Florida lawmakers using tax dollars to fund institutions that propagate their personal religious beliefs � lawmakers map a slippery slope to a de facto �Theocracy�. Claims that deserving institutions that provide valuable social or healthcare services are unfairly deprived of public funding are bogus, since many nonprofit organizations affiliated with religious groups (i.e. Catholic Charities) already receive public funding under the current law � provided they do not promote their religion. Using language from failed voucher bills, lawmakers plan this as a thinly veiled vehicle for diverting public education funds to private schools that espouse and promote the lawmaker�s own religious beliefs. Naming the Amendment �Religious Freedom� is roughly akin to the congressional deregulation bills that stripped away air and water quality standards while cynically entitled �The Clean Air Act� and �Saving our Waterways Act.� The cherry on top of this wingding is an enigmatic absence of accountability. A $50,000 allocation to the Messianic Tabernacle of the Hairy Eyeball can be used to stock up on AK-47s � without impact.

Amendment 9: Homestead Property Tax Exemption for Surviving Spouse of Military Veteran or First Responder

-

Amendment 9 would grant a full property tax exemption to the surviving spouses of military veterans who die while on active duty and to those of first responders who die in the line of duty. Amendment 9 would grant a full property tax exemption to the surviving spouses of military veterans who die while on active duty and to those of first responders who die in the line of duty.  Since State law already granted this property tax exemption to eligible military spouses in 1997, the amendment extends the exemption to the surviving spouses of law enforcement officers, correctional officers, firefighters, emergency medical technicians and paramedics who die in the line of duty and enshrines the benefit in the Florida Constitution. Taxpayers would have to cough up an additional $600,000 annually ($2.4 million over four years) to offset the loss of revenues to local governments ($300,000/year) and schools ($300,000/year). (HJR 93 � sponsored in 2012 by Sen. Jim Norman, R-Tampa, and Rep. Shawn Harrison, R-Temple Terrace) Since State law already granted this property tax exemption to eligible military spouses in 1997, the amendment extends the exemption to the surviving spouses of law enforcement officers, correctional officers, firefighters, emergency medical technicians and paramedics who die in the line of duty and enshrines the benefit in the Florida Constitution. Taxpayers would have to cough up an additional $600,000 annually ($2.4 million over four years) to offset the loss of revenues to local governments ($300,000/year) and schools ($300,000/year). (HJR 93 � sponsored in 2012 by Sen. Jim Norman, R-Tampa, and Rep. Shawn Harrison, R-Temple Terrace)

Amendment 10: Tangible Personal Property Tax Exemption

Amendment 11: Additional Homestead Exemption; Low-Income Seniors Who Maintain Long-Term Residency on Property; Equal to Assessed Value

Amendment 11 would give an additional property tax exemption to low-income seniors who have lived in their home for more than 25 years. (HJR 169 � sponsored in 2012 by Sen. Rene Garcia, R-Hialeah, and Rep. Jose Oliva, R-Hialeah/Miami) Amendment 11 would give an additional property tax exemption to low-income seniors who have lived in their home for more than 25 years. (HJR 169 � sponsored in 2012 by Sen. Rene Garcia, R-Hialeah, and Rep. Jose Oliva, R-Hialeah/Miami)

- Seniors who meet income criteria and own homes valued under $250,000 can fully exempt their properties from all but school taxes. The Amendment would cost local governments $27.8 million over 3 years.

Amendment 12: Appointment of Student Body President to Board of Governors of the State University System

Amendment 12 would change the way the state selects the student representative on the state university system�s Board of Governors, which oversees the university system. (HJR 931 � sponsored in 2012 by Sen. Bill Montford, D-Apalachicola, and Rep. Matt Gaetz, R-Shalimar) Amendment 12 would change the way the state selects the student representative on the state university system�s Board of Governors, which oversees the university system. (HJR 931 � sponsored in 2012 by Sen. Bill Montford, D-Apalachicola, and Rep. Matt Gaetz, R-Shalimar)

- The president of the Florida Student Association (FSA) currently serves on the State University System�s 17-member Board of Governors. This amendment would create a new council composed of student body presidents, and the chair of that council would replace the current FSA representative on the Board of Governors.

- You should be wondering �What in hell is this?� A sour grapes amendment by Florida State (FSU), since FSU chose not to participate in the Florida Student Association, creating a new panel will give it a shot at power. While clearly more appropriate to a campus fraternity survey sponsored by the Political Science Department, it also serves to clarify that the lawmakers who formulated these amendments opted to ignore the nature and purpose of a State Constitution.

In Summary

Hoping to maneuver the electorate into endorsing causes that resonate with party leaders, our Republican lawmakers buried an evisceration of privacy rights in an anti-abortion amendment and mischaracterized an amendment that blots out the separation between Church and State as �Religious Freedom�. Since approval of an anti-�Obamacare� amendment would theoretically place in the Florida Constitution an endorsement to violate federal law, which is unconstitutional, it only serves to take a swing at the incumbent Presidential candidate. Finally, an amendment that provides the Legislature with additional power over the Judiciary specifically places that power in the hands of the majority party. Hoping to maneuver the electorate into endorsing causes that resonate with party leaders, our Republican lawmakers buried an evisceration of privacy rights in an anti-abortion amendment and mischaracterized an amendment that blots out the separation between Church and State as �Religious Freedom�. Since approval of an anti-�Obamacare� amendment would theoretically place in the Florida Constitution an endorsement to violate federal law, which is unconstitutional, it only serves to take a swing at the incumbent Presidential candidate. Finally, an amendment that provides the Legislature with additional power over the Judiciary specifically places that power in the hands of the majority party.

To distract attention from these thorny ideological blisters, the majority leadership merged them with amendments bloated with tax exemptions for questionably deserving sub-groups of highly sympathetic segments of our population. These giveaways would be far more appropriate if offered when State and local economies weren�t clawing their way out of a recession. By forcing local governments to hand out new or expanded financial gifts to veterans from other states, landlords, wives of first responders, vacation homes, seniors, and virtually anyone that doesn�t already have a homestead exemption, they will also force local public officials to pay for this by increasing tax rates and transferring the additional financial burden to YOU! Alternatively, they could always close more parks and libraries. To distract attention from these thorny ideological blisters, the majority leadership merged them with amendments bloated with tax exemptions for questionably deserving sub-groups of highly sympathetic segments of our population. These giveaways would be far more appropriate if offered when State and local economies weren�t clawing their way out of a recession. By forcing local governments to hand out new or expanded financial gifts to veterans from other states, landlords, wives of first responders, vacation homes, seniors, and virtually anyone that doesn�t already have a homestead exemption, they will also force local public officials to pay for this by increasing tax rates and transferring the additional financial burden to YOU! Alternatively, they could always close more parks and libraries.

Topping these off with inane amendments creating a new student council and a spending cap that was either rejected by or failed in every state where it was considered speaks to the absence of any legitimate reason to affix them in our Constitution. If you are concerned about becoming confused when finally facing a ballot filled with indecipherable political doubletalk, simply ask yourself �Do I want to pay for this?� Make no mistake � we will! Topping these off with inane amendments creating a new student council and a spending cap that was either rejected by or failed in every state where it was considered speaks to the absence of any legitimate reason to affix them in our Constitution. If you are concerned about becoming confused when finally facing a ballot filled with indecipherable political doubletalk, simply ask yourself �Do I want to pay for this?� Make no mistake � we will!

Click To Top of Page

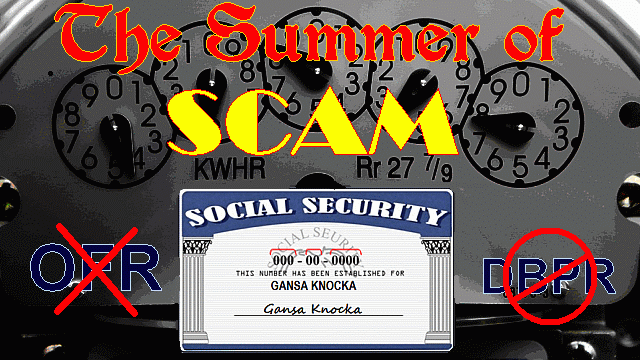

October 12, 2012 - An eclectic group of sleaze bags logged in substantial overtime this summer. Each of the following scams either threatened or victimized Galt Milers during the stickiest June through August in years. Thousands of cash-strapped utility customers were stung by a low-tech nationwide fraud using a hook based on the weather, the political climate, Facebook and the �allure of the freebie�. Another scam targeted the men and women who manage our homes, threatening their license and livelihood. The last one, conceived by our clever Governor, will insure that the State of Florida maintains its squirrelly reputation as the nation�s mortgage fraud �Olympian� while the Venice of America perseveres as �Fraud Lauderdale.� October 12, 2012 - An eclectic group of sleaze bags logged in substantial overtime this summer. Each of the following scams either threatened or victimized Galt Milers during the stickiest June through August in years. Thousands of cash-strapped utility customers were stung by a low-tech nationwide fraud using a hook based on the weather, the political climate, Facebook and the �allure of the freebie�. Another scam targeted the men and women who manage our homes, threatening their license and livelihood. The last one, conceived by our clever Governor, will insure that the State of Florida maintains its squirrelly reputation as the nation�s mortgage fraud �Olympian� while the Venice of America perseveres as �Fraud Lauderdale.�

Obama Utility Scam hits South Florida

A new twist on an old sting recently cut a coast to coast swath of victims. In late spring, the Better Business Bureau (BBB) issued a nationwide fraud warning about a scam imputing that �President Obama will pay your utility bills through a new federal program.� First reported on the BBB website on June 15th, these highly organized crooks used fliers, social media and text messages to assert that President Obama sponsored a bailout to relieve the fiscal strain placed on homeowners by serial heat waves and a struggling economy. Upon registering for the program by submitting their social security and bank routing numbers, consumers received a Federal Reserve Bank routing number with which they could pay their utility bills using the company�s automated payment service. Of course � the routing number was a fake. A new twist on an old sting recently cut a coast to coast swath of victims. In late spring, the Better Business Bureau (BBB) issued a nationwide fraud warning about a scam imputing that �President Obama will pay your utility bills through a new federal program.� First reported on the BBB website on June 15th, these highly organized crooks used fliers, social media and text messages to assert that President Obama sponsored a bailout to relieve the fiscal strain placed on homeowners by serial heat waves and a struggling economy. Upon registering for the program by submitting their social security and bank routing numbers, consumers received a Federal Reserve Bank routing number with which they could pay their utility bills using the company�s automated payment service. Of course � the routing number was a fake.

Every year, variations of this scam bag a few hundred self-deluded prayer warriors. This year was different. Exploiting a confluence of disparate events, the perpetrators tweaked the traditional hoax, significantly ramping up returns. The early summer heat waves, bloated utility bills, a flat lining economy and the slime-packed nationwide campaign tripe pumped out by Romney and Obama supporters gave the scam teeth. To enhance the scam�s credibility, the crooks carefully researched standard utility payment protocols. When a bogus routing number is fed to a power company�s automated payment service, the utility will initially acknowledge the bill as paid. Of course, when they discover that the account is vapor, the charges are reinstated. Every year, variations of this scam bag a few hundred self-deluded prayer warriors. This year was different. Exploiting a confluence of disparate events, the perpetrators tweaked the traditional hoax, significantly ramping up returns. The early summer heat waves, bloated utility bills, a flat lining economy and the slime-packed nationwide campaign tripe pumped out by Romney and Obama supporters gave the scam teeth. To enhance the scam�s credibility, the crooks carefully researched standard utility payment protocols. When a bogus routing number is fed to a power company�s automated payment service, the utility will initially acknowledge the bill as paid. Of course, when they discover that the account is vapor, the charges are reinstated.

Unlike similar scams that wholly rely on digital delivery, this was distinguished by a complementary human element. While a target community is flooded with emails, tweets and Facebook messages about the fictitious program, agents hired by the scammers go house to house, handing out leaflets and posting flyers that encourage potential marks to register for the non-existent federal credits. Planned with military precision, scammers moved quickly through a neighborhood. By the time victims � and the local utility � learned about the scam, the crooks were off to a new playing field � often in another state. To frame the hoax with realistic production values, paid solicitors wore utility company uniforms. Fast evolving variations of the scam offered similar �credits� to pay cell phone charges, credit card debt and cable television bills. Spokesperson Katherine Hutt for the Better Business Bureau�s national office in Washington, D.C. explored the possibility that the solicitors who were hired by the crooks were ignorant of their complicity in a rip-off. Unlike similar scams that wholly rely on digital delivery, this was distinguished by a complementary human element. While a target community is flooded with emails, tweets and Facebook messages about the fictitious program, agents hired by the scammers go house to house, handing out leaflets and posting flyers that encourage potential marks to register for the non-existent federal credits. Planned with military precision, scammers moved quickly through a neighborhood. By the time victims � and the local utility � learned about the scam, the crooks were off to a new playing field � often in another state. To frame the hoax with realistic production values, paid solicitors wore utility company uniforms. Fast evolving variations of the scam offered similar �credits� to pay cell phone charges, credit card debt and cable television bills. Spokesperson Katherine Hutt for the Better Business Bureau�s national office in Washington, D.C. explored the possibility that the solicitors who were hired by the crooks were ignorant of their complicity in a rip-off.

The current incarnation of this fraud seems to have begun in Texas, when Dallas-based Atmos Energy reported that customers were first hoodwinked in mid-May. In New Jersey, Public Service Electric & Gas (PSE&G) later reported that 10,000 customers were stung by the scam. In early July, 2000 TECO Energy customers in Tampa were swindled. The grifters also worked communities in North Carolina, Pennsylvania, Utah, California, Indiana, and multiple jurisdictions in New England and Florida. Florida Power & Light spokesman Neil Nissan estimated that 30,000 of FPL�s 4.5 million customers had fallen victim by Independence Day. Upon learning that their customers were victimized, affected utilities added fraud warnings to their automated telephone payment systems and customer websites for online bill payments. To help cushion those already stung, utilities in Tampa and New Jersey agreed to waive late fees and postpone service interruption. Other victims may not be as lucky. Thousands of other utility customers who remain unaware of the rip-off may first learn about it when their electricity is suddenly disconnected. Surprised by the scam�s unanticipated traction, TECO spokeswoman Sylvia Wood commented �We see scams once or twice a year, and a handful of people fall for them. But this is crazy.� The current incarnation of this fraud seems to have begun in Texas, when Dallas-based Atmos Energy reported that customers were first hoodwinked in mid-May. In New Jersey, Public Service Electric & Gas (PSE&G) later reported that 10,000 customers were stung by the scam. In early July, 2000 TECO Energy customers in Tampa were swindled. The grifters also worked communities in North Carolina, Pennsylvania, Utah, California, Indiana, and multiple jurisdictions in New England and Florida. Florida Power & Light spokesman Neil Nissan estimated that 30,000 of FPL�s 4.5 million customers had fallen victim by Independence Day. Upon learning that their customers were victimized, affected utilities added fraud warnings to their automated telephone payment systems and customer websites for online bill payments. To help cushion those already stung, utilities in Tampa and New Jersey agreed to waive late fees and postpone service interruption. Other victims may not be as lucky. Thousands of other utility customers who remain unaware of the rip-off may first learn about it when their electricity is suddenly disconnected. Surprised by the scam�s unanticipated traction, TECO spokeswoman Sylvia Wood commented �We see scams once or twice a year, and a handful of people fall for them. But this is crazy.�

Another reason for the scam�s explosive impact was its instant popularity as a social media cherry. Convinced that they were beneficiaries of a legitimate government grant, victims enthusiastically told family, friends and neighbors about the easy money. When a reasonably skeptical Galt Mile woman who learned about the bogus program from a friend�s tweet called in the accompanying bank routing number to FP&L, the utility�s automated service confirmed her balance due as zero. Overnight, thousands of Facebook pages featured glowing accounts of the President�s consumer utility bailout. Fooled by the scam�s well-scripted �hook�, Pro-Romney websites condemned President Obama for wasting scarce federal resources on �social entitlements.� Thousands of tweets bore witness to the imaginary governmental largesse, as duped customers circulated hundreds of fake routing numbers they just fed to FP&L, Metro PCS, National Grid in New England, TECO, Duke Energy, and dozens of other utility vendors. Another reason for the scam�s explosive impact was its instant popularity as a social media cherry. Convinced that they were beneficiaries of a legitimate government grant, victims enthusiastically told family, friends and neighbors about the easy money. When a reasonably skeptical Galt Mile woman who learned about the bogus program from a friend�s tweet called in the accompanying bank routing number to FP&L, the utility�s automated service confirmed her balance due as zero. Overnight, thousands of Facebook pages featured glowing accounts of the President�s consumer utility bailout. Fooled by the scam�s well-scripted �hook�, Pro-Romney websites condemned President Obama for wasting scarce federal resources on �social entitlements.� Thousands of tweets bore witness to the imaginary governmental largesse, as duped customers circulated hundreds of fake routing numbers they just fed to FP&L, Metro PCS, National Grid in New England, TECO, Duke Energy, and dozens of other utility vendors.

Upon receiving an emailed invitation to register, even savvy web-surfers who ordinarily trash marketing spam were hooked by the tweeted �success stories�, eagerly joining the fast-growing list of victims. Describing how social media ebullience added fuel to the prospect of getting a free ride, PSE&G spokeswoman Bonnie Sheppard said �Once it morphed into the social media thing, it just kept getting passed on from friend to friend to friend.� Upon receiving an emailed invitation to register, even savvy web-surfers who ordinarily trash marketing spam were hooked by the tweeted �success stories�, eagerly joining the fast-growing list of victims. Describing how social media ebullience added fuel to the prospect of getting a free ride, PSE&G spokeswoman Bonnie Sheppard said �Once it morphed into the social media thing, it just kept getting passed on from friend to friend to friend.�

The scam left three classes of victim in its wake. Marks who �registered� by handing over their Social Security and Banking data not only took a fiscal hit, but must run a painful gauntlet to reclaim their identity. Although they aren�t at risk for Identity Theft, those who paid bills with fake routing numbers lifted from Twitter or Facebook pages may still have to cough up some late fees while recovering from mildly bruised egos. Additionally, victims who mistakenly believe that their bills are paid may awaken to a refrigerator filled with rotting food. The scam left three classes of victim in its wake. Marks who �registered� by handing over their Social Security and Banking data not only took a fiscal hit, but must run a painful gauntlet to reclaim their identity. Although they aren�t at risk for Identity Theft, those who paid bills with fake routing numbers lifted from Twitter or Facebook pages may still have to cough up some late fees while recovering from mildly bruised egos. Additionally, victims who mistakenly believe that their bills are paid may awaken to a refrigerator filled with rotting food.

While generally applicable, PT Barnum�s classic observation that a sucker is born every minute doesn�t explain why so many people suddenly decided to ignore the well-publicized dangers of divulging their Social Security and Banking data in return for a month-long respite from their utility bills. While generally applicable, PT Barnum�s classic observation that a sucker is born every minute doesn�t explain why so many people suddenly decided to ignore the well-publicized dangers of divulging their Social Security and Banking data in return for a month-long respite from their utility bills.

Unlike wildly lucrative digital thefts wherein crooks programmed invasive computer malware to strip corporate databases of $billions in sensitive financial information, this low-tech operation relied on tactical familiarity with internet marketing strategies, corporate protocols, large group dynamics, and social networking. Timing the scam to target utilities during a heat wave amid a tough economy was no accident. By camouflaging a bogus federal entitlement as a campaign enticement, the scammers provided an eminently credible hook. Flexible and mobile, before corporate security or law enforcement authorities could get a fix on events, the scammers evaporated overnight and resurfaced in the next city or state. Unlike wildly lucrative digital thefts wherein crooks programmed invasive computer malware to strip corporate databases of $billions in sensitive financial information, this low-tech operation relied on tactical familiarity with internet marketing strategies, corporate protocols, large group dynamics, and social networking. Timing the scam to target utilities during a heat wave amid a tough economy was no accident. By camouflaging a bogus federal entitlement as a campaign enticement, the scammers provided an eminently credible hook. Flexible and mobile, before corporate security or law enforcement authorities could get a fix on events, the scammers evaporated overnight and resurfaced in the next city or state.

Snopes.com, a website devoted to exposing and categorizing hoaxes, credits the scam�s success to the fact that �It seems to work,� referring to the payment confirmations offered by utilities after initially processing a customer�s fake check routing number. They also offer examples of the social media entries that helped turn a mildly destructive scam into a nationwide blight. What seems to most tantalize fraud �editorialists� is the carefully scripted human element � the decision to seal the deal with door to door dupes. Snopes.com, a website devoted to exposing and categorizing hoaxes, credits the scam�s success to the fact that �It seems to work,� referring to the payment confirmations offered by utilities after initially processing a customer�s fake check routing number. They also offer examples of the social media entries that helped turn a mildly destructive scam into a nationwide blight. What seems to most tantalize fraud �editorialists� is the carefully scripted human element � the decision to seal the deal with door to door dupes.

Concerned that scam victims who read their website may suffer from denial, after affirming the existence of government programs that assist low-income households with their utility bills, Snopes.com bursts the balloon, �There is no government program that provides blanket grants to cover everyone�s utility bills in full for a whole month.�

Galt Mile CAM Managers Placed on Alert

On October 6, Community Advocacy Network (CAN) Executive Director Donna Berger emailed an alert to Galt Mile Associations. The popular Association Attorney�s notice was reprinted from the Department of Business and Professional Regulation (DBPR) website. Evidently, another group of moderately ambitious scammers are targeting license holders. On the Galt Mile, that means the men and women who oversee the daily operation of our homes � Community Association Managers. As compared to the well-oiled Obama hoax, this soggy donut borders on the insipid. On October 6, Community Advocacy Network (CAN) Executive Director Donna Berger emailed an alert to Galt Mile Associations. The popular Association Attorney�s notice was reprinted from the Department of Business and Professional Regulation (DBPR) website. Evidently, another group of moderately ambitious scammers are targeting license holders. On the Galt Mile, that means the men and women who oversee the daily operation of our homes � Community Association Managers. As compared to the well-oiled Obama hoax, this soggy donut borders on the insipid.

| DBPR SECRETARY

KEN LAWSON |

An unsolicited email which appears to be from the Department warns of some pending disciplinary action against license holders. The email directs the recipient to �call a Department investigator at a toll-free number and provide personal identification information.� One local property manager said �Since trained managers are familiar with Identity Theft, I seriously doubt they found many victims, especially along the Galt Mile. Frankly, anyone who falls for this transparent scam isn�t qualified to manage an Association.� DBPR Secretary Ken Lawson isn�t so sure. He circulated the warning to hundreds of companies and advocacy organizations representing scores of fields licensed by the Agency. An unsolicited email which appears to be from the Department warns of some pending disciplinary action against license holders. The email directs the recipient to �call a Department investigator at a toll-free number and provide personal identification information.� One local property manager said �Since trained managers are familiar with Identity Theft, I seriously doubt they found many victims, especially along the Galt Mile. Frankly, anyone who falls for this transparent scam isn�t qualified to manage an Association.� DBPR Secretary Ken Lawson isn�t so sure. He circulated the warning to hundreds of companies and advocacy organizations representing scores of fields licensed by the Agency.

Tom Grady � The Fraud Friendly Hatchet

It shouldn�t come as a surprise that Florida leads the nation in mortgage fraud. Incredibly, Florida Governor Rick Scott decided to address the state�s blackened reputation by decimating the state agency that fights mortgage fraud. On August 2, 2011, Governor Scott strolled down the block from his Naples home to visit neighbor Tom Grady, a millionaire securities lawyer and stockbroker who served in the Florida House from 2008 to 2010. A few days later, Scott named Grady Commissioner of the Office of Financial Regulation (OFR) with marching orders to gut the Agency. It shouldn�t come as a surprise that Florida leads the nation in mortgage fraud. Incredibly, Florida Governor Rick Scott decided to address the state�s blackened reputation by decimating the state agency that fights mortgage fraud. On August 2, 2011, Governor Scott strolled down the block from his Naples home to visit neighbor Tom Grady, a millionaire securities lawyer and stockbroker who served in the Florida House from 2008 to 2010. A few days later, Scott named Grady Commissioner of the Office of Financial Regulation (OFR) with marching orders to gut the Agency.

| TOM GRADY AND LT. GOV. JENNIFER CARROLL PARTY

WITH ANN SCOTT, THE WIFE OF GOV. RICK SCOTT |

Two weeks later, Grady praised an investigator in the agency�s Pensacola office who helped crack a $3 million mortgage fraud scheme. After telling reporters �Thanks to (her) leadership, the OFR is doing its part to put bad guys behind bars,� Grady closed the Pensacola office at 4900 Bayou Boulevard and gave her the boot. In short order, Grady canned 81 other OFR investigators and support personnel while closing regional offices in Fort Myers, Jacksonville, Pensacola and Fort Lauderdale. Ironically, the Venice of America has served as ground zero to so many financial scams that it has long been known to State and Federal investigators as �Fraud Lauderdale�

| | OFR DEP. COMM. GREG HILA |

Grady wasn�t finished neutering the State�s primary bastion against fiscal fraud. Seeking to groom his future replacement at the Agency, Grady dumped a veteran Division Director and installed Greg Hila, a Naples Chiropractor turned Real Estate Agent and one of Scott�s golfing buddies. Since state law mandates that the OFR commissioner have some minimal experience with securities and finance, when Grady left OFR, the Financial Services Commission barred Hila from filling his shoes. Instead, former Financial Institutions Director Linda Charity was named Interim Commissioner. The fact that this unqualified Chiropractor is currently the Agency�s Deputy Commissioner is an inside joke in Tallahassee.

| | ATTORNEY PETER KING |

With a severely crippled regional outreach and amateurs loyal to the Governor managing damage control in Tallahassee, Grady needed a dog and pony show. He would replace the ousted enforcement professionals with an all-volunteer panel of securities attorneys and charge them with detecting securities fraud. In a news release, Grady said that these private sector lawyers would be �our eyes and ears throughout the state � to help put bad guys behind bars and help good guys succeed.� To co-chair the panel, Grady named Tampa Attorney Peter King and Scott Link, a partner in the West Palm Beach law firm of Ackerman, Link & Sartory. As explained by Link in a subsequent interview, �We�re not regulators and can only refer matters to state regulators � not investigate, subpoena or arrest anyone.� In short, the panel is window dressing.

| | ATTORNEY SCOTT LINK |

| | BANK ANALYST KEN THOMAS |

After King and Link recruited 12 colleagues, on March 2, 2012, Grady announced the formation of his 14-member �Advisory Council.� Other than some telephone contacts, the panel has never met. When apprised of Grady�s amateur fraud-busters, independent Miami banking analyst Ken Thomas commented �This is unbelievable. Grady is going to use lawyers to be his eyes and ears on the ground? What do you do if one of his eyes and ears is representing Rothstein, Madoff or Stanford (convicted legendary scam artists Scott Rothstein, Bernard �Bernie� Madoff and Allen Stanford)?�

| FORMER OFR COMM.

TOM GRADY |

Thomas was referring to �Attorney-Client Privilege�, a legal concept that protects certain communications between clients and their attorneys and keeps those communications confidential. A crook need only hire one of the private-sector Attorneys on the Advisory Council to preclude them from sharing privileged evidence of guilt, thereby turning the Office of Financial Regulation into a get-out-of-jail-free card. Satisfied that the dismantled Agency could no longer threaten �entrepreneurs� like Rothstein, Scott asked Grady to do a repeat performance at Citizens Insurance. Four days after announcing the bogus Advisory Council, Grady was named interim President at Citizens. After watching Grady run up $10,000 in travel expenses in five weeks, including stays in Bermuda and Amelia Island, an embarrassed Citizens Board pink slipped the gubernatorial hatchet two weeks later. Thomas was referring to �Attorney-Client Privilege�, a legal concept that protects certain communications between clients and their attorneys and keeps those communications confidential. A crook need only hire one of the private-sector Attorneys on the Advisory Council to preclude them from sharing privileged evidence of guilt, thereby turning the Office of Financial Regulation into a get-out-of-jail-free card. Satisfied that the dismantled Agency could no longer threaten �entrepreneurs� like Rothstein, Scott asked Grady to do a repeat performance at Citizens Insurance. Four days after announcing the bogus Advisory Council, Grady was named interim President at Citizens. After watching Grady run up $10,000 in travel expenses in five weeks, including stays in Bermuda and Amelia Island, an embarrassed Citizens Board pink slipped the gubernatorial hatchet two weeks later.

| | TAMPA ATTORNEY GUY BURNS |

When Scott first approached Grady about taking a wrecking ball to the OFR, he had a problem. Six years earlier, Grady and Tampa Attorney Guy Burns were hired by the State Board of Administration (SBA) to sue the New York money management firm Alliance Capital Management for losing $300 million in State Pension Funds they invested in Enron, the failed energy company. When a jury found for Alliance, the SBA signed a pact with Alliance agreeing that neither side would appeal the decision.

With the action retired by a jury, Grady and Burns billed the SBA for $1.4 million in questionable fees for travel and lodging, computer research and copier services (as per court documents). The SBA refused to pay the unconscionably excessive fees, citing a contingency clause in their legal contract requiring a �favorable� courtroom result for payment of legal services. Five years later, days before the statute of limitations would expire, the lawyers sued the State. With the action retired by a jury, Grady and Burns billed the SBA for $1.4 million in questionable fees for travel and lodging, computer research and copier services (as per court documents). The SBA refused to pay the unconscionably excessive fees, citing a contingency clause in their legal contract requiring a �favorable� courtroom result for payment of legal services. Five years later, days before the statute of limitations would expire, the lawyers sued the State.

Since Scott, CFO Jeff Atwater and Attorney General Pam Bondi serve as Trustees for the State Board of Administration; Grady had to assign his stake in the case to co-plaintiff Burns in order to camouflage the conflict and snag the $133,000 job. Announcing Grady�s appointment, Scott said �He has demonstrated a high standard of integrity in all he has done and holds a deep commitment to serving the people of Florida.� He didn�t mention that Grady was also suing the people of Florida. Since Scott, CFO Jeff Atwater and Attorney General Pam Bondi serve as Trustees for the State Board of Administration; Grady had to assign his stake in the case to co-plaintiff Burns in order to camouflage the conflict and snag the $133,000 job. Announcing Grady�s appointment, Scott said �He has demonstrated a high standard of integrity in all he has done and holds a deep commitment to serving the people of Florida.� He didn�t mention that Grady was also suing the people of Florida.

| | LEXISNEXIS JENNIFER BUTTS |

Grady claimed that no one would notice the State�s crippled enforcement capabilities because the economic downturn has diminished the number of companies writing mortgage loans. A July Report by LexisNexis Risk Solutions confirms that Florida still leads the nation in mortgage fraud, with an increased incidence rate since Grady�s departmental massacre. Spokesperson Jennifer Butts of LexisNexis commented �I think Florida�s shutdown of regional offices goes against the grain,� and prompted the need for �many other regulators outside Florida to increase scrutiny.�

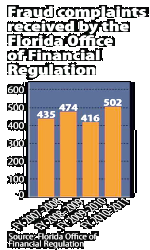

To elicit legislative approval for disemboweling the only State Agency fighting mortgage fraud, Grady told lawmakers that �the number of open investigations has fallen 58 percent since the end of 2010.� The tricky doggie omitted having received 502 fraud complaints in OFR�s fiscal year 2011, up from 416 the year before. Federal investigators, the BSO and the Broward State Attorney�s Office expressed disbelief and frustration over the Administration�s willingness to manufacture data in furtherance of a policy that shields mortgage and securities fraud, crimes that are particularly devastating to Florida�s fixed-income retirees. To elicit legislative approval for disemboweling the only State Agency fighting mortgage fraud, Grady told lawmakers that �the number of open investigations has fallen 58 percent since the end of 2010.� The tricky doggie omitted having received 502 fraud complaints in OFR�s fiscal year 2011, up from 416 the year before. Federal investigators, the BSO and the Broward State Attorney�s Office expressed disbelief and frustration over the Administration�s willingness to manufacture data in furtherance of a policy that shields mortgage and securities fraud, crimes that are particularly devastating to Florida�s fixed-income retirees.

Understandably fearful of Administration reprisals, State law enforcement officials walk on eggshells because of the Governor�s personal experience with government fraud investigators, many of whom were among those recently �downsized� by his axe man. Rick Scott presided over healthcare goliath Columbia/HCA when the FBI raided his offices in 1997 as part of a Medicare and Medicaid fraud investigation. In the largest case of healthcare fraud in U.S. history, the Justice Department fined Columbia/HCA $1.7 billion for 14 felonies, while Scott got a pass for stepping down as Chairman and CEO. Six days before announcing his gubernatorial candidacy, Scott lied to regulators when deposed in a case investigated by the Florida Department of Law Enforcement (FDLE) wherein his new company, Solantic Urgent Care centers, defrauded Medicare. After curing the violations with his checkbook, state sleuths were still investigating discrimination charges against Solantic when Scott slid into the Governor�s Mansion and sold the company to New York investment group Welsh, Carson, Anderson & Stowe � who partnered with healthcare executive Michael Klein to rebrand Solantic as Care-Spot Express Healthcare and relocate its headquarters to Nashville. Understandably fearful of Administration reprisals, State law enforcement officials walk on eggshells because of the Governor�s personal experience with government fraud investigators, many of whom were among those recently �downsized� by his axe man. Rick Scott presided over healthcare goliath Columbia/HCA when the FBI raided his offices in 1997 as part of a Medicare and Medicaid fraud investigation. In the largest case of healthcare fraud in U.S. history, the Justice Department fined Columbia/HCA $1.7 billion for 14 felonies, while Scott got a pass for stepping down as Chairman and CEO. Six days before announcing his gubernatorial candidacy, Scott lied to regulators when deposed in a case investigated by the Florida Department of Law Enforcement (FDLE) wherein his new company, Solantic Urgent Care centers, defrauded Medicare. After curing the violations with his checkbook, state sleuths were still investigating discrimination charges against Solantic when Scott slid into the Governor�s Mansion and sold the company to New York investment group Welsh, Carson, Anderson & Stowe � who partnered with healthcare executive Michael Klein to rebrand Solantic as Care-Spot Express Healthcare and relocate its headquarters to Nashville.